Chargeback Shopify

Chargeback Prevention for Shopify Subscription Brands: Stop Disputes Before They Start

Chargeback prevention Shopify brands need. Intercept pre-disputes, reduce fees, and protect recurring subscription revenue before escalation.

Online payment disputes are projected to reach $28.1 billion in 2026. And subscription businesses are hit the hardest.

Most Shopify brands discover their chargeback problem 30 days too late. By then, the dispute has escalated, the fees are locked in, and your payment processor relationship is already under pressure. If you run a membership or subscription program, the stakes are even higher. Recurring charges are the most disputed transaction type in ecommerce, and every unresolved dispute chips away at the revenue you worked hard to build.

The good news is that most chargebacks are avoidable. Effective chargeback prevention for subscription and membership brands is not about fighting disputes after the fact. It is about intercepting them before they ever become chargebacks at all.

What Is a Chargeback, and Why Should Subscription Brands Care?

A chargeback happens when a customer disputes a charge directly with their bank rather than contacting you. The bank investigates, and if they side with the customer, the transaction is forcibly reversed. You lose the revenue, you are charged a dispute fee, and the incident is counted against your chargeback rate with your payment processor.

Unlike a standard refund, which you control, a chargeback is initiated outside your store entirely. You have no window to resolve it before the reversal happens. And regardless of whether you ultimately win the dispute, it still counts against you.

Subscription and membership brands carry extra exposure here. Recurring charges are easy for customers to forget. Billing descriptors can look unfamiliar months after sign-up. Many customers simply go to their bank when they want to cancel rather than using your portal. Each of those counts as a dispute, not a cancellation, and each one repeats at scale.

The Refund Is the Smallest Part of the Bill

When a dispute becomes a chargeback, the financial impact goes well beyond the refund itself. The true cost hits your business in four compounding ways: lost merchandise you cannot recover, chargeback fees that stack on top of the reversed transaction, processing penalties from your payment processor as your dispute rate climbs, and long-term risk to your account if rates stay elevated.

Each chargeback incident typically carries a dispute fee between $15 and $100 on top of the lost transaction value. Your dispute rate rises with your processor. If rates stay elevated, you risk being placed in a monitoring program, which brings additional fees, enhanced scrutiny, and restrictions on your account. In serious cases, your ability to accept card payments altogether can be suspended.

Card networks like Visa operate formal monitoring programs with defined thresholds. For example, under the Visa Fraud Monitoring Program, brands enter an early warning tier around 0.65% dispute rates, move into a standard tier at roughly 0.9%, and can be classified as excessive at 1.8% or higher. Once in the standard or excessive tiers, fines can reach $50 per chargeback, and if rates remain elevated for consecutive months, additional penalties or even account termination may follow. The gap between 0.9% and 1.8% is not incremental. It is the difference between stability and financial escalation.

Friendly fraud, meaning legitimate customers disputing charges they actually authorized, accounts for a significant share of all chargebacks. Subscription brands are disproportionately affected because recurring charges are both high in volume and low in customer awareness. If someone forgot they signed up, or if they expected an email before being billed, the path of least resistance is a call to their bank.

This is why chargeback prevention cannot be an afterthought. It needs to be built into how you run your retention programs from day one.

Prevention Starts Before the Bank Gets Involved

The key to stopping chargebacks is understanding the timeline. A chargeback happens when a customer disputes a charge with their bank and the bank formally processes that claim. But before that formal processing, there is a pre-dispute window where intervention is still possible.

Visa and Mastercard both operate alert programs that notify merchants the instant a dispute signal is detected. When a brand catches a dispute at this pre-dispute stage, they can resolve it directly, typically by issuing an automatic refund, before a chargeback is ever filed. A refunded pre-dispute does not count against your chargeback rate. That distinction matters enormously for brands managing recurring revenue at scale.

Proactive, not reactive. Catch disputes early. Resolve them before escalation. That is the entire model.

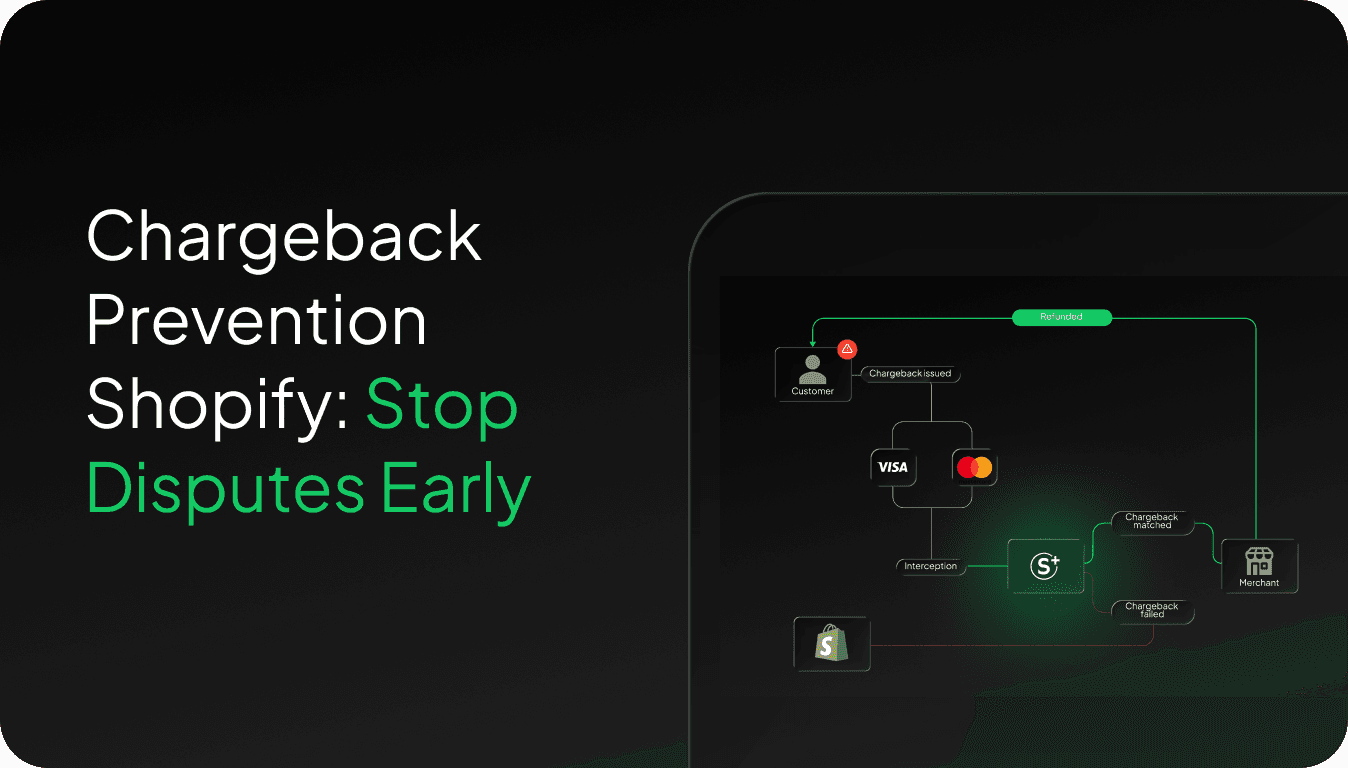

How Subscribfy Intercepts Disputes Before Shopify Ever Sees Them

Subscribfy connects directly with Visa and Mastercard to detect early dispute signals. When a dispute is flagged, order details are sent automatically to the issuing bank. Most disputes are resolved at that stage, before they ever reach your Shopify account.

The system matches flagged disputes to the correct Shopify orders with 90% accuracy using AI-powered order matching. This reduces errors and gives you the clarity to act quickly. Across our client base, Subscribfy intercepts around 95% of chargebacks before they hit your account.

The difference in numbers is significant. Brands running without chargeback prevention often see dispute rates around 1.8%. With Subscribfy running, that number drops to 0.2%. The gap between those two figures is the difference between account risk and account health.

You Set the Rules. The System Does the Work.

One of the most common concerns brands have about automated chargeback prevention is loss of control. The worry is that disputes will be refunded automatically in cases where you could have won. Subscribfy is built to address exactly that.

Brands set simple automation rules upfront. Low-risk disputes below a defined threshold are refunded automatically, canceling them before they escalate. Higher-value or higher-risk cases are flagged for manual review. You define the thresholds, the risk criteria, and the response actions. The system handles execution.

This approach keeps your dispute rate low, reduces the manual workload on your CX team, and protects your standing with your payment processor. Everything is visible in a real-time dashboard with Slack alerts, so nothing slips through unnoticed.

Why Chargeback Prevention Belongs Inside Your Retention Platform

What makes Subscribfy different from a standalone chargeback tool is that dispute prevention is built into the same platform running your memberships, subscriptions, and loyalty programs. Dispute interception, order matching, and automated resolution work together inside one system, alongside the programs generating the recurring revenue you are protecting.

This matters because chargebacks are not a payment operations problem in isolation. They are a recurring revenue problem. Every dispute you do not catch early costs you twice: the refund, and the fees and processor risk that follow. Brands protecting their revenue have stopped treating chargebacks as an unfortunate cost of doing business and started building prevention into how they run retention.

If your membership or subscription program is driving meaningful recurring revenue, chargeback prevention is not optional. It is the infrastructure that lets that revenue compound safely over time.

Want to see how Subscribfy prevents chargebacks across your membership and subscription programs? See how we protect recurring revenue for Shopify Plus brands.

Frequently Asked Questions About Chargeback Prevention for Subscription Brands

What is the difference between a chargeback and a refund?

A refund is initiated by you, the merchant. You choose to return a customer's money and the process stays within your control. A chargeback is initiated by the customer through their bank, entirely outside your store. You have no opportunity to resolve it before the reversal happens, and it is counted against your chargeback rate with your payment processor regardless of the outcome.

Why are subscription and membership brands more vulnerable to chargebacks?

Recurring charges are the most disputed transaction type in ecommerce. Customers forget they signed up. Billing descriptors look unfamiliar months after sign-up. Many members go straight to their bank when they want to cancel rather than using a self-serve portal. Each of these scenarios generates a dispute rather than a cancellation, and each one counts against your chargeback rate.

What is friendly fraud and how does it affect subscription businesses?

Friendly fraud happens when a legitimate customer disputes a charge they actually authorized. For subscription brands, this typically looks like a customer forgetting about a renewal, disputing a charge after already using a perk, or going to their bank instead of canceling through your portal. Because subscription billing is recurring, a single customer can generate multiple chargebacks before the account is resolved, compounding the damage to your dispute rate.

What is a pre-dispute and why does it matter?

A pre-dispute is the moment a customer contacts their bank to question a charge, before the bank formally processes it as a chargeback. Visa and Mastercard both operate alert programs that notify merchants at this stage. If a merchant resolves the dispute during this window, typically by issuing a refund, it does not count as a chargeback against their rate. This pre-dispute window is where automated chargeback prevention does its most important work.

Book a meeting with our sales team now!

Create predictable revenue from the customers you already have.